Canada-China Trade: Q2 2023

Daniel Lincoln and Karel Brandenbarg - 13 October 2023

*Revised December 11, 2023

The trend of increased Canadian exports to China and decreased imports from China to Canada - on a year-over-year (YoY) basis - which was observed in Q4 2022 and Q1 2023 has continued over the course of Q2 2023. However, the rate of this growth in exports has decreased and the rate of import contraction has accelerated since Q1 2023, indicating an increasingly uncertain macroeconomic environment in both China and Canada.

Unlike Q1 2023, Q2 2023 has seen the Canadian trade deficit with China increase, which is on track to grow further. While Canadian exports to China have experienced growth on an annual basis compared to low exports in 2022 amid China’s Zero-Covid policy, exports are on a downward trend when looking at monthly data for H1 2023. This trend indicates that the Canadian trade deficit with China will likely continue to grow for the remainder of the year, as it is largely driven by the faltering of China’s post-Covid economic recovery that started in Q2 2023.

The following data is gathered from Statistics Canada for goods (merchandise) trade with China, presented on an unadjusted customs basis in Canadian dollars (CAD). The relevant HS 4-digit identification code is used to identify product groups. All values are in Canadian dollars (CAD).[1]

Canada-China Trade: Q2 2023

Exports:

Source: Trade Data Online (Statistics Canada – Customs Data)

Source: Trade Data Online (Statistics Canada – Customs Data)

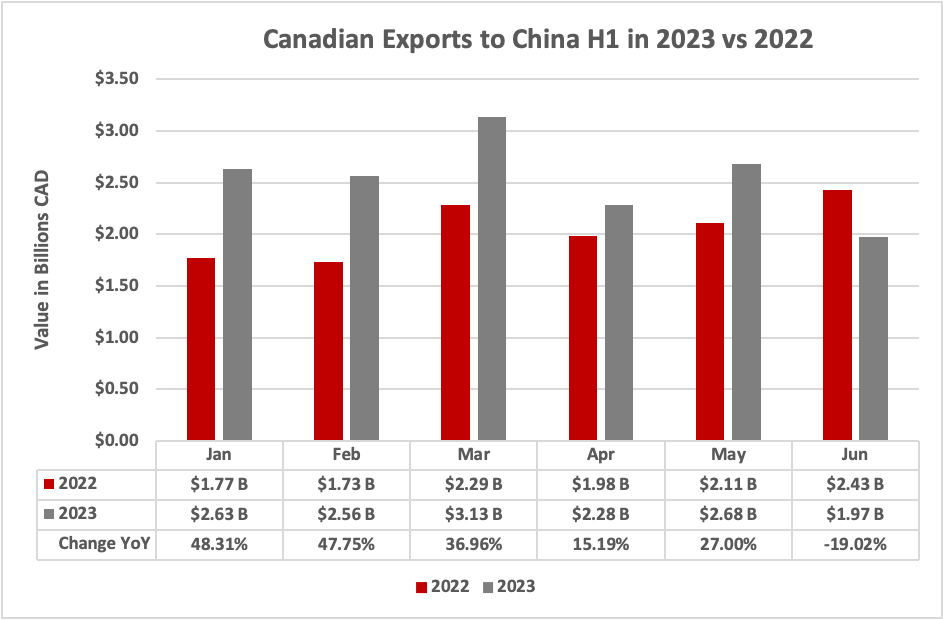

The first half of 2023 has seen Canadian export growth to China significantly outpace growth in Canadian exports to other countries. The growth rate of exports to China was 23.85% year-over-year (YoY), with a value of $15.26 billion. Meanwhile, Canadian exports to other countries contracted by -0.82% in the same period YoY, amounting $367.64 billion. The decrease in Canadian exports to countries other than China can largely be explained by the increasing global economic downturn, whereas the simultaneous growth in exports to China is affected by many factors, including the specific set of commodities Canada exports to China. As seen in the graph below, exports grew YoY in April and May but decreased substantially in June, indicating slowing export growth and perhaps even contraction going forward into 2023.

Source: Trade Data Online (Statistics Canada – Customs Data)

In H1 2023, Canada’s leading HS4 export to China was canola,[2] with a value of $2.28 billion, showcasing an impressive YoY growth of 301.49%. Following canola was coal,[3] the second-largest export to China, totalling $1.50 billion, but experiencing a significant YoY contraction of -31.00%. The third-ranking Canadian export to China was chemical wood pulp,[4] valued at $1.20 billion, reflecting a strong YoY growth rate of 22.11%. In the fourth spot was iron,[5] amounting to $1.10 billion and demonstrating a robust 16.06% YoY growth rate. Finally, Canada’s fifth-largest export to China was copper,[6] totalling $650.28 million, but it faced a YoY contraction of -8.25%.

Imports:

Source: Trade Data Online (Statistics Canada – Customs Data)

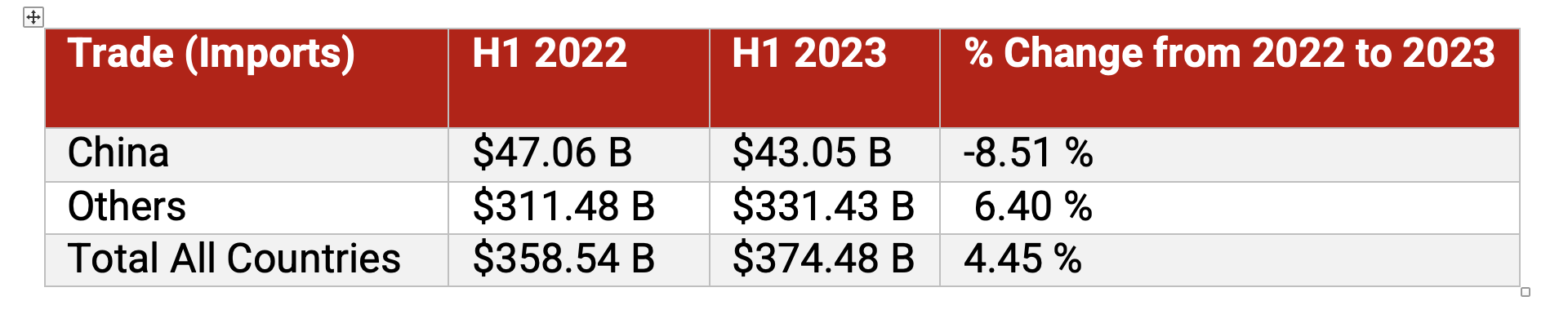

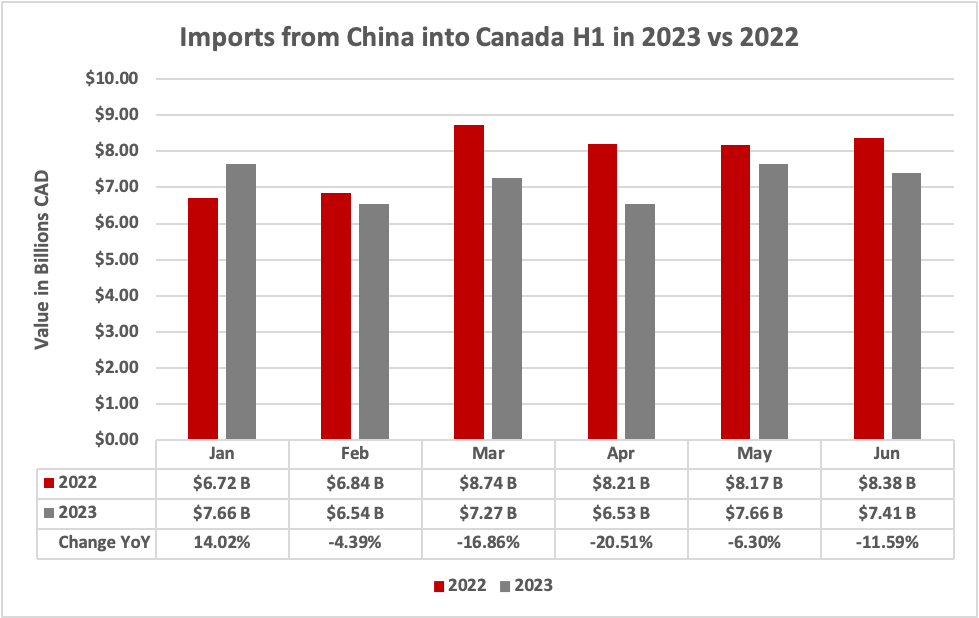

Canadian imports from China throughout H1 2023 followed the trend seen in Q1 2023, wherein imports from China shrank as imports from other countries grew. While Canada’s imports from all countries other than China totalled $331.43 billion and exhibited a 6.40% YoY growth rate, Canadian imports from China were valued at $43.05 billion and contracted by -8.51%. Every month in Q2 saw lower imports from China YoY, with April exhibiting the largest contraction of the quarter at -20.51% YoY. This trend is largely indicative of both Canadian demand and Chinese supply being subdued due to macroeconomic issues in both countries.

Source: Trade Data Online (Statistics Canada – Customs Data)

Canada’s foremost HS4 product category imported from China was cellphones,[7] with a total value of $3.87 billion, demonstrating a modest YoY growth rate of 3.88%. Following this was the second-largest import from China, automatic data processing machines (e.g., computers),[8] which amounted to $3.07 billion but experienced a significant contraction of -22.10% YoY. The third-ranking import category was heaters,[9] value at $1.48 billion, impressively showcasing a YoY growth of 198.92%. In the fourth position were vehicle parts,[10] accounting for $1.17 billion and displaying a healthy 8.79% YoY growth. Finally, the fifth-largest import category was non-medical furniture,[11] totalling $812.74 million but contracting by -18.28% YoY.

Canada-China Trade: Last 24 months

Source: Trade Data Online (Statistics Canada – Customs Data)

The last 24 months of bilateral Sino-Canadian trade indicate several key trends within the trade relationship. Although Q1 saw Canada’s trade deficit diminishing slightly, it grew in Q2. While imports have fluctuated month-to-month between growth and contraction, Canadian exports to China slowed, resulting in an increase in the trade deficit compared to Q1 2023. A negative trajectory in import growth is evident given the substantially lower level of imports compared to most of 2022. Despite overall YoY growth in Canadian exports to China, export growth is slowing from its pace in Q1 2023 with signs in June that exporting to China may further cool and may even contract this year. This trend would return the trade balance to be more in line with overall trends as the last year saw a unique decrease in the trade deficit.

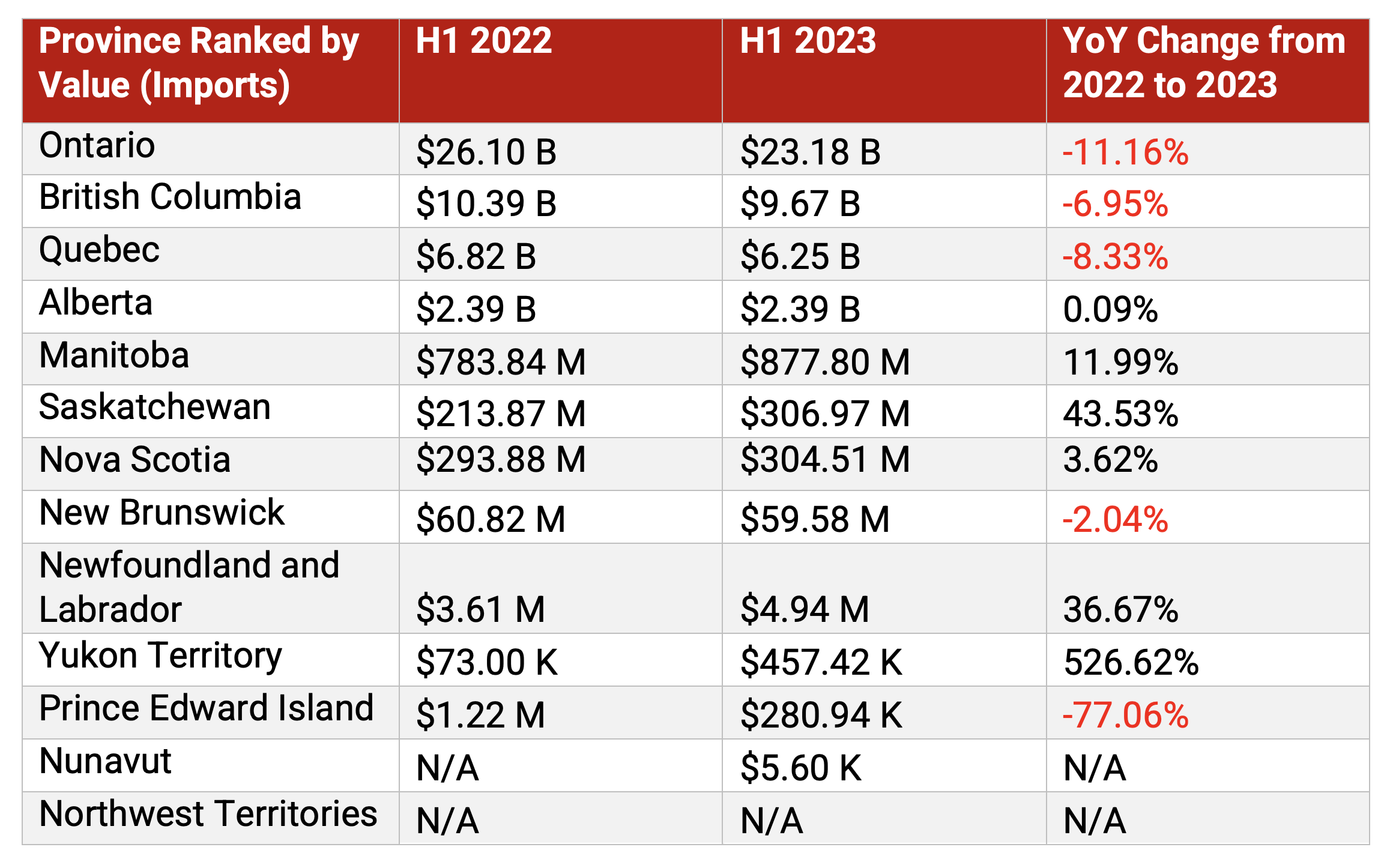

Q2 2023 Canada-China Trade: By Province/Territory

Notation as follows: Billion (B), Million (M), Thousands (K)

Source: Trade Data Online (Statistics Canada – Customs Data)

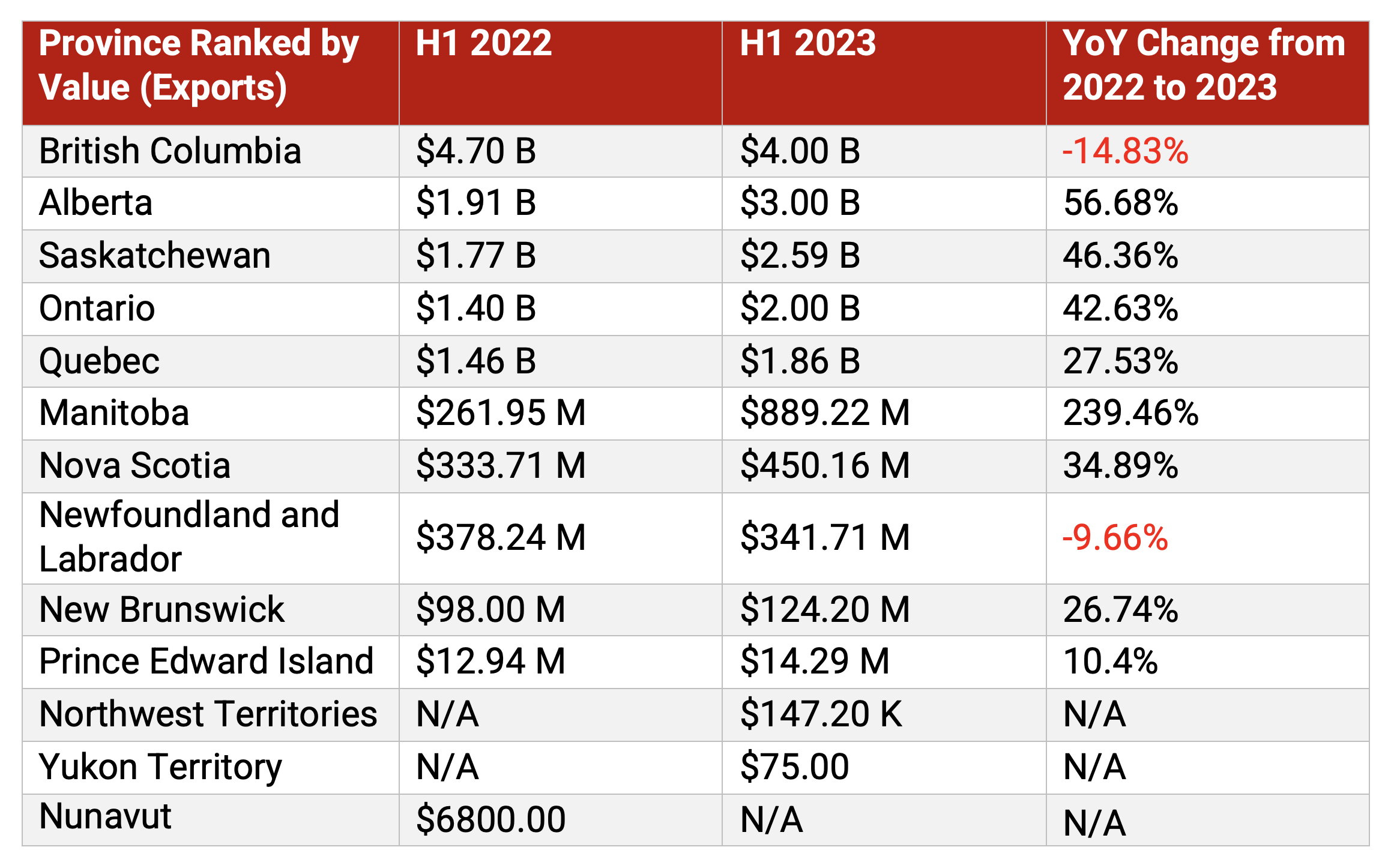

In line with trends on a national scale, most provinces saw a YoY growth in exports to China, while Canada’s most populous provinces experienced contractions in imports from China. British Columbia was an outlier insofar as it was the only province to experience a YoY decline in both exports (-14.83%) and imports (-6.95%). While strong export growth was observed in both Ontario (42.63%) and Quebec (27.53%), both provinces experienced contractions in imports, -11.16% and -8.33%, respectively. This contraction has been caused at least partially by high indebtedness and lower consumer spending amid rising interest rates. The decrease in imports from China in Quebec and Ontario has contributed significantly to the decrease in overall imports from China on a national level given their large share of Canada’s total population. However, the prairie provinces of Alberta, Saskatchewan, and Manitoba all experienced strong growth in exports, driven by resource extraction and agriculture industries. Manitoba, in particular, experienced an astounding 239.46% growth in exports to China and positive import growth of 11.99% YoY as well. Notably, Yukon Territory is an outlier in imports from China, experiencing a YoY growth of 526.62%, although the total value of these imports was a modest $457,417.

Trends & Topics

The Consumer Squeeze: Canadian Economic Troubles Accumulate as Consumers Struggle with High Debt and Inflation

Over the course of Q2 2023, multiple signs of economic stress have continued to mount in the Canadian economy. Although the Canadian economy performed better than expected in Q1 2023, exhibiting a growth of 2.6% in real GDP YoY, the second quarter saw a 0.2% YoY contraction. With persistent inflation prompting the Bank of Canada to continuously hike interest rates, consumer confidence has decreased significantly during Q2 due largely to high levels of indebtedness. Regardless of the efforts of the Bank of Canada to cool inflation, inflation has remained higher than expected in Q2 and is predicted to stay elevated throughout the remainder of 2023.

Canada currently faces economic challenges marked by the highest household debt among the G7 nations, despite the Bank of Canada raising interest rates. Persistent inflation coupled with increasing debt payments has raised concerns, leading to a relatively unpredictable macroeconomic landscape. In Q2, a significant portion of Canadians found housing costs challenging, contributing to a worsened financial position for 46% of the population. This economic strain is reflected in Q2 retail sales data, showing a decrease of 0.8%, reflecting likely diminished consumer confidence. The high cost of living and reduced demand for mortgages have also contributed to an 8.2% drop in new construction, impacting Canada's construction and real estate industries and contributing to a GDP contraction.

These factors have likely had an adverse effect on Canadian imports from China. The annualized contraction in Canadian imports from China has increased in H1 2023, with a -4.06% decrease in Q1 2023 accelerating to a -8.51% cumulative reduction by the end of H1. Since a significant portion of Canada’s imports from China constitute retail goods, a decrease in consumer confidence caused by indebtedness and inflation means that many Canadians are spending less on such Chinese imports. This is evidenced particularly by a significant slowing in the growth rate for key imports from China, compared to Q1. For example, while cellphone imports grew 10.78% in Q1 YoY, their total growth for H1 stands at only 3.88% YoY. Likewise, water heater imports grew by 762.76% in Q1 as opposed to 198.82% for H1 as a whole, and non-medical furniture has contracted further in H1, from -10.61% YoY in Q1 to -18.28% by the end of H1. The slowing growth in water heater imports and growing contraction in non-medical furniture imports have at least partially been caused by a decrease in residential construction and renovations in Q2. It is likely that as inflation and high debt levels continue to take their toll on Canadian consumers, this trend of decreased discretionary spending on retail goods causing a decrease in overall imports from China will persist.

A Rocky Recovery - China’s Post-Pandemic Economy Slows amid Global Economic Woes

The first quarter of 2023 indicated a positive outlook for China’s post-pandemic economic recovery, with strong consumer demand and GDP growth. However, China’s impressive Q1 performance has not persisted into Q2, with the increased services consumption that the Chinese economy experienced in Q1 being far outweighed by other mounting economic woes. Decreased demand both at home and abroad has dealt a blow to China’s post-COVID economic recovery. Consumers abroad have cut their household spending and increased their savings in anticipation of a looming recession, and Chinese consumers have started to decrease their discretionary spending amid a cooling property market and record-high youth unemployment. These external and internal pressures have caused the Chinese economy to grow by only 0.8% in Q2 relative to Q1, which was lower than expected. This was not contained to Mainland China, as Hong Kong saw slower growth in Q2 (1.5% YoY), than in Q1 (2.9% YoY), indicating that the economic downturn is affecting the Greater China region.

Although the problems facing the Chinese economy were less severe in Q2 than they have been in Q3 thus far, the cracks that formed throughout Q2 had a significant effect on China’s trade with foreign countries, including Canada. In terms of Canadian exports to China, the annualized rate of growth in H1 2023 slowed to 23.85%, as opposed to 44.21% in Q1, which indicates that exports to China slowed in Q2. This slowed growth is consistent with decreasing global demand over the course of 2023, as growth in Canadian exports to all other countries also contracted significantly in the same period, from 8.71% in Q1 to -0.82% by the end of H1. This strong early growth was driven by China’s reopening from COVID. The YoY growth rate for the top five Canadian export categories to China have all slowed in Q2 relative to Q1, with some experiencing accelerated contraction. For example, coal contracted by -13.85% YoY in Q1, which increased to -31.00% for H1. Likewise, Q1 saw a YoY growth of 27.16% in copper, which had reversed to a cumulative annualized contraction of -8.25% by the end of H1.

These trends are both indicative of larger macroeconomic troubles currently affecting China. Steadily decreasing Canadian coal exports to China are largely caused by both the contraction in domestic industrial production and alternative coal suppliers. The contraction in Canadian copper exports to China is significant insofar as copper demand is viewed by economists as a proxy for global growth, thus the downturn in Chinese imports of Canadian copper not only indicates a downturn in China’s economy, but also in the broader global economy. As annualized growth in Canadian exports to China remain strong – largely due to the export of essential consumer goods, such as the previously banned canola – compared to exports to other countries, the rate of growth has significantly decreased over the course of H1, which mirrors increasing economic troubles in China. Given that China’s domestic economic environment has further weakened as of the publication of this article, the outlook for year-end performance in these areas is less optimistic.

It is worth noting that other countries have also experienced a downturn in imports of Chinese goods in Q2, including large developed economies. For example, the United States is currently facing a potential recession, which in turn has resulted in decreased American consumer demand. This has contributed to a significant drop in US imports of Chinese goods throughout H1 2023, as many of the Chinese goods imported by the US are consumer goods. Similarly, China itself has experienced decreased domestic demand. These factors have manifested in a contraction in Chinese industrial output in Q2. This phenomenon illustrates that these macroeconomic issues are not confined to Canada-China bilateral trade, but rather reflect broader trends in the global economy amid the recovery from COVID-19.

Looking forward, several economic issues will affect China’s trade relationship with Canada. Firstly, China’s domestic economy has continued to face challenges in Q3, with analysts repeatedly downgrading their short-term outlook for China’s economy, but has also seen an uptick in the Purchasing Manger Index (PMI), which indicates some optimism for industrial output. These mixed signals make the future of bilateral trade uncertain which adds risk for investors. Secondly, the World Bank predicts that future economic growth in China will be subdued, projected at 4.6% in 2024 and 4.4% in 2025, largely due to the maturation of China’s economy from a labour-intensive manufacturing hub into a high-tech and advanced manufacturing economy. Thirdly, China’s ongoing transition towards a high-tech economy means that Canadian consumers will rely on China less as a source for many cheap consumer goods, which forms a significant share of total Chinese exports to Canada. Finally, as economists predict that global growth will be far slower in the 2020s than it was in previous decades, this may cause both global and Canadian demand for Chinese exports to decrease.

A Dangerous Dance: Diplomatic Tensions Continue to Impede Economic Relations

Political tensions accelerated significantly over the course of Q2 2023, arguably eclipsing the heightened hostilities in past quarters. Further allegations of foreign interference in Canada by China, simmering tensions in the Indo-Pacific region, and increasing diplomatic hostility have all contributed to significant geopolitical tensions between the West and China in Q2 2023. In particular, these tensions have manifested themselves economically, with Canada and other Western countries increasingly viewing their close economic relationship with China as a liability amid rising geopolitical tensions.

Domestic developments in Q2 saw Canadian media again spotlight foreign interference. Leaked CSIS reports in May heightened concerns, accusing China of targeting Canadian MPs critical of its domestic and international policies. In May, Canada expelled a Chinese diplomat, which triggered reciprocal actions by the Chinese government. Political turmoil ensued, leading to calls for a public inquiry into foreign interference. Special rapporteur David Johnston's resignation, prompted by perceived ties to China, added complexity to the issue. This ongoing saga, continuing into Q3, strained Sino-Canadian relations, and was intensified by RCMP closures of alleged covert Chinese police stations in Canada.

On the global stage, Sino-Canadian relations also deteriorated amid heightened geopolitical tensions in the Indo-Pacific region during Q2. Canada has begun to adopt a more confrontational stance towards China, expressing intent to join AUKUS and increase its military presence in the Indo-Pacific. The June USS Chung-Hoon and HMCS Montreal incident underscored the growing adversarial role Canada assumes against China in coordination with Western allies, intensifying strain on Sino-Canadian ties. Furthermore, Prime Minister Justin Trudeau’s statements that specifically condemned countries including Russia and China have exacerbated these tensions and illustrate Canada’s increasingly assertive opposition to perceived geostrategic competitors.

These ongoing political factors which are currently troubling Sino-Canadian relations are becoming increasingly intertwined with economics, and will likely have a significant effect on Canada’s trade relationship with China going into the future. Already Canada has explicitly identified their economic relationships with China as a tool in navigating geopolitical tensions. During Q2, the Canadian government has again emphasized the importance of “friendshoring” (i.e., increasing trade ties with allies), and G7 diplomats called for economic “de-risking” from China during their summit in late May. The impact of geopolitical tensions on trade is illustrated by the accelerating US-China tech war, which has seen both countries placing targeted trade sanctions on each other’s technological industries on national security grounds. Canada has taken steps during Q2 to decrease its trade reliance on China, with Seoul and Ottawa signing a critical minerals deal amid a drive to increase cooperation with geopolitically-friendly “reliable partners”. Moreover, Canada paused its participation in the Asian Infrastructure Investment Bank (AIIB) pending a review, due to the belief that it is “dominated” by the CCP, indicating a willingness to sever economic ties due to geopolitical hostility.

In general, the greatest current risk to economic relations between Western countries and China is the unpredictability that is generated by simmering geopolitical tensions. This uncertainty has manifested itself throughout Q2.The Chinese stock market’s performance was hampered in Q2 by geopolitical conflict between the West and China, which in turn contributed to unpredictability in the value of the yuan. Furthermore, major fund managers during Q2 have pulled out of companies that are viewed as being vulnerable amid these growing geopolitical tensions, such as Taiwan Semiconductor Manufacturing Company Ltd. (TSMC).

Although a single quarter is not enough to infer a paradigm shift in trade relations between Canada and China as caused by geopolitical tensions, the fact that hostilities between Western countries and China have continued to accelerate in Q3 and show little sign of cooling off portends a continuation of this trend for the foreseeable future. This represents the manifestation of trends that have been previously noted in past trade reports -- that is, an increasingly tumultuous and unpredictable geopolitical environment could culminate in decreased trade and investment between Canada and China. It should be noted that total Canada-China bilateral trade hit an all-time high last year despite high tensions, however, at the midpoint of 2023 the current annual outlook appears weaker. Therefore, although macroeconomic issues in both Canada and China negatively impacted trade in Q2 2023, geopolitical tensions are exerting an increasingly adverse effect on trade relations as well, which is a factor that will likely persist for the remainder of 2023.

[1] Please note that some sums and percentage points may not add up perfectly on tables and graphs due to rounding.

[2] HS4 product group: 1205 – Rape or Colza Seeds (Whether or Not Broken)

[3] HS4 product group: 2701 – Coal and Solid Fuels Manufactured from Coal

[4] HS4 product group: 4703 – Chemical Woodpulp – Soda or Sulphate

[5] HS4 product group: 2601 – Iron Ores and Concentrates

[6] HS4 product group: 2603 – Copper Ores and Concentrates

[7] HS4 product group: 8517 – Telephone Sets; Other Apparatus For Trans/Recep of Voice/Image/Data, O/T 84.43, 85.25, 85.27, 85.28

[8] HS4 product group: 8471 – Adpm & Units, Magnetic/Optical Readers, Machine Transcribing Data To Media in Code & To Process

[9] HS4 product group: 8419 – Non-Domestic Dryers and Temperature Changing Apparatus; Instantaneous Water Heaters

[10] HS4 product group: 8708 – Motor Vehicle Parts (Excl. Body, Chassis and Engines)

[11] HS4 product group: 9403 – Furniture – Other than For Medical, Surgical or Dental Use

Authors

Daniel Lincoln

Policy Research Assistant

Daniel is a recent graduate of the University of Alberta, completing a BA With Distinction in Political Science, Economics, and History. Daniel also received a Certificate in Globalization and Governance that he completed in conjunction with his undergraduate degree. His primary research interests include Russian and Chinese foreign policy, international trade, security policy, and Canada's geopolitical and economic role in the Arctic.

Karel Brandenbarg

Policy Research Assistant

Karel graduated from the BA Honors program at the University of Alberta with a major in Political Science and double minor in Economics and Philosophy. His honor thesis focused on the ethical implications of realist International Relations theory.