Budget Model 2.0

The University of Alberta’s budget model directs how the university organizes revenues and costs. A budget model does not generate revenue or extra funds for the university, it simply distributes those funds. Good models incentivize choices that grow revenues in future years.

A new model was designed in 2023 for use in the Budget 2024-2025 cycle.

Changing Models

Since the previous budget model was developed, the university has been impacted by cuts to operating grant funds of $222 million (34%).

Beyond this, the previous model had four limitations in its ability to effectively steer us towards the University of Alberta for Tomorrow (UAT) goals.

The previous model:

- leaves units overly exposed to funding shocks, which have been experienced over the past three years

- limits our capacity for long-term planning, with planning dominated by year-on-year changes in government grants

- does not secure stable funding for university-wide strategic initiatives, which are critical to our future success

- does not create the right incentives with respect to enrollment growth, teaching and research

Fiscal year 2025-26 model:

- creates incentives with respect to our growth and research targets

- supports us to plan ahead, rather than responding to year-over-year fluctuations in the operating grant

- ensures that our limited resources are directed in a way that achieves the goals stated in UAT

- provides a level of transparency and clarity into the university budget that can enable fully informed decision making.

The New Model

The new model helps achieve the goals of Shape: The University Strategic Plan 2023-2033 by incentivizing our growth and research through three primary levers. Faculty Deans will receive allocated funding and are still responsible for allocating to the department level with each of the faculties.

Revenue and Grant Allocation

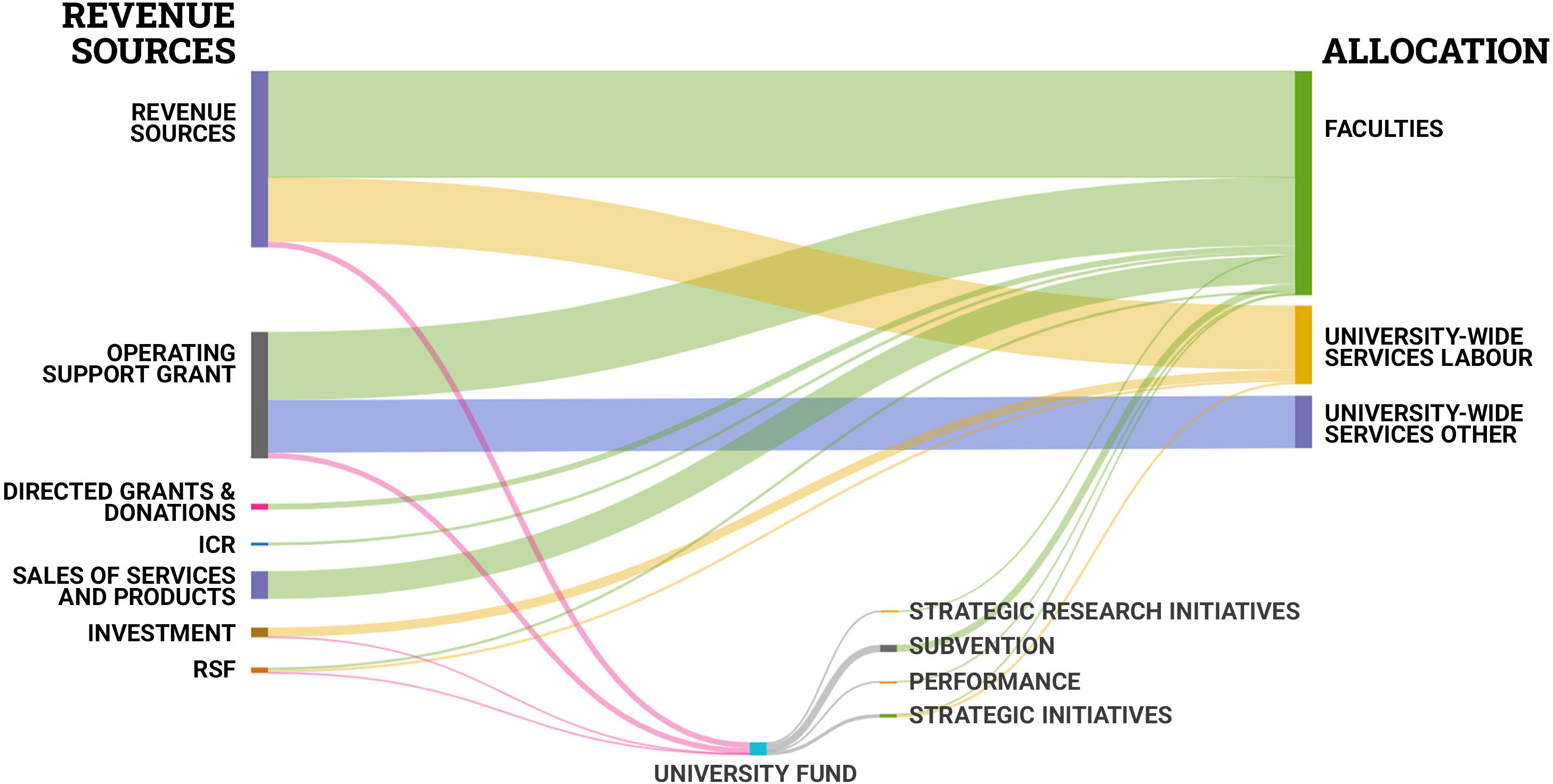

Inputs of the budget model, otherwise known as revenue sources, include tuition revenue, operating support grants, directed grants and donations, ICR, sales of services and products, investment and RSF. The outputs of these sources are then allocated to faculties and university-wide services. The largest revenue sources for the university are tuition revenue and the operating support grant. A small proportion of revenue is directed into a ‘University Fund’ pool, these funds are then distributed out via four different funds: a strategic research initiatives fund (SRIF), subvention fund, performance fund, and strategic initiatives fund (SIF).

The below Sankey diagram represents the inputs and outputs of the budget model. The diagram is for illustration purposes only, it does not represent the accurate distribution nor is it based on real figures.

See a Sankey diagram of the revenue and grant allocation based on Budget Model 2.0 »

The diagram is for illustration purposes only; it does not represent the accurate distribution nor is it based on real figures.

The transition plan was confirmed as the proposed 5-year straight-line approach. Resource Planning, the Provost and VP USF will continue to collect feedback from faculties and units throughout implementation in fiscal year 2025-26 to inform future iterations of the model.

Model Levers

Lever 1: Enrollment

Enrolment drives tuition revenues and allocation of the Operating and Programming Support Grants and Tuition funding

Lever 2: Research Growth

Research growth drives allocation of the Research Support Fund (RSF) Grant and the Operating and Programming Support Grant.

Lever 3: Faculty efficiency and effectiveness

Teaching load and fill rates are examples of levers for managing costs relative to enrolment revenue.

For more information on the current model please review the Budget Model 2.0 Information Paper.

What’s Next

The model’s comprehensive design process helped produce a new model that will best achieve the university’s goal, but there are still some decisions remaining. The model has been approved for fiscal year 2025-26 and there are still some changes to be considered for fiscal year 2026-27 and onwards.

Working Groups

Several decisions still remain, so we have established two small working groups focused on refining the Faculty Cost Clusters (FCC) and institutional space cost elements of the budget model. Additional working groups are being considered for other areas of the Budget Model.

Faculty Cost Cluster Working Group

As part of Budget Model 2.0, the university transitioned to Faculty Cost Clusters (FCC). FCCs seek to benchmark the cost of programming against domestic and international universities to support a simple and transparent process.

When the FCCs were announced for fiscal year 2025-26, academic leaders from faculties and colleges expressed the need for a more comprehensive and data-driven approach. An accurate and trusted set of FCCs is integral to the success of the university.

To mitigate these risks, an FCC Working Group of academic leaders and administrative subject matter experts has been established to refine the FCCs for the Fiscal Year 26 budget process.

The FCC Working Group will:

- Advise Resource Planning on relevant data sources to inform each faculty’s FCC.

- Develop a plan to collect effective benchmark figures on cost of programming to inform FCCs in future budget cycles.

- Develop an approach for periodic review of FCCs.

- Advise leadership on changes to the FCCs for the fiscal year 2025-26 and future years.

Space Optimization Working Group

Effective space optimization practices are integral to achieving Shape: The University Strategic Plan 2023-2033. Ineffective space use can unnecessarily increase the cost of operating space and distort the university’s long term infrastructure needs. Through this, it can hinder the university’s ability to advance research and teaching activities, and limit the university’s potential to grow enrolment and research.

A Space Optimization Working Group has been established to decide how the university’s space assets can meet the university’s needs and free up resources to support growth.

The Space Optimization Cost Working Group will engage with university leaders to:

- Agree on the most effective use of space assets to drive positive and impactful behaviour change over the long-term that supports the university's goals.

Model Review

We are committed to continuing to review Budget Model 2.0. No one Budget Model is perfect, nor can they be designed with perfect information. We commit to reviewing the model regularly as information arises, including a formal model review in 2028, following three years of use.

Should you have questions about the university’s budget model, you can contact the Budget Model Team at budget@ualberta.ca.